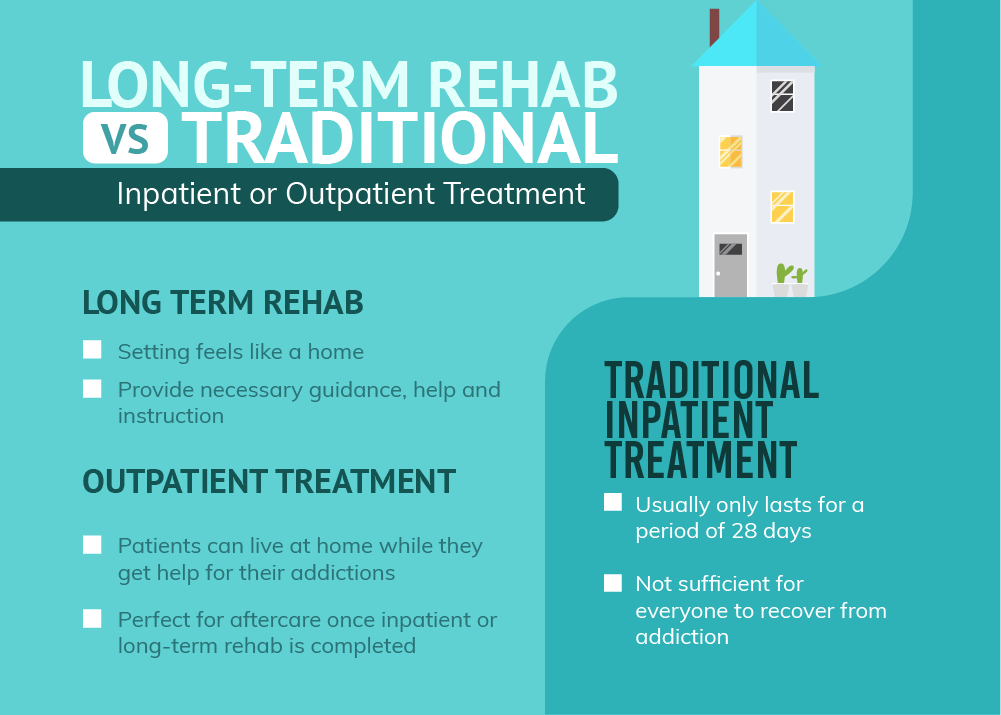

If the job is completed to the extent of the project as well as to state and also neighborhood codes, money is launched to pay the contractor. The Federal Real Estate Management (FHA) 203( k) rehabilitation lending or Fannie Mae HomeStyle Renovation Home mortgage could be great funding choices for purchasers seeking fixer-uppers. These lendings permit you to purchase the home with a get that's put in escrow to fund remodellings. Car loans for flipping tasks are extra costly than house purchase fundings. The rates of interest is greater, and you might need to pay numerous factors or origination charges.

Can a first time home buyer get a rehab loan?

FHA 203(k) Rehabilitation mortgages allow first-time homebuyers to take advantage of below-market interest rate loans that cover costs of purchasing and making full or limited renovations to your dream home. This program may also be used to finance abandoned or foreclosed properties.

Do you need a downpayment for a rehab loan?

Down payment: The minimum down payment for a 203(k) loan is 3.5% if your credit score is 580 or higher. You'll have to put down 10% if your credit score is between 500 and 579. Down payment assistance may be available through state home buyer programs, and monetary gifts from friends and family are permitted as well.

Take time to make a decision just how much house you can actually afford and afterwards finance as necessary. If you can afford to place a significant quantity down or have enough revenue to create a reduced LTV, you will have much more negotiating power with loan providers as well as one of the most financing choices. If you promote the biggest funding, you might be offered a greater risk-adjusted price as well as private home mortgage insurance policy.

Common and also limited 203( k) lendings have different regulations about how much you can obtain for renovations and what you can do with the cash. Improvements the FHA regards deluxes, like a pool or outdoor kitchen area, generally aren't eligible. You require to identify specialists who can do the job when you've chosen you desire to apply for a combination loan for your remodelling as well as acquisition.

Acquiring an FHA 203k home mortgage may seem complex, however if your cash reserves are low or you don't have a lot of home equity, it might be your finest choice. Just make sure to look around for a lending institution with lots of 203k experience so that you can avoid difficulties with the loan. And make sure the contractor you choose additionally has 203k mortgage experience so they recognize what the FHA program may require in terms of evaluations as well as receipts for proof the work has been done. With this program you can locate on your own with the kitchen of your dreams as well as a month-to-month home loan repayment you can afford. The most significant distinction in receiving an FHA 203k home mortgage instead of a standard FHA mortgage is that you have to qualify based upon the costs of your remodelling, along with the purchase price.

- All FHA debtors pay ahead of time home loan insurance policy, no matter how much residence equity they have or the size of their down payment, which raises the size of the monthly settlement.

- FHA car loans are exceptional for first-time homebuyers since, along with reduced ahead of time funding prices and also much less rigorous credit rating requirements, you can make a down payment as low as 3.5%.

- Division of Real Estate as well as Urban Development, supplies various mortgage programs.

- An FHA funding has lower down payment requirements and also is simpler to get approved for than a conventional finance.

PMI insulates the lender from default by transferring a section of the lending danger to a home mortgage insurer. A lot of loan providers call for PMI for any finance with an LTV more than 80%, implying any type of financing where you own less than 20% equity in the house.

How do you qualify for a rehab loan?

Rehab mortgages are a type of home improvement loans that can be used to purchase a property in need of work -- the most common of which is the FHA 203(k) loan. These let buyers borrow enough money to not only purchase a home, but to cover the repairs and. renovations a fixer-upper property might need.

However prior to we dive into the particular mortgage loan kinds, allow's rapidly specify a couple of vital concepts that apply to all the numerous types. Acquiring a residence for the very first time can be challenging, specifically when you begin researching all the various lending options readily available to make that residence a reality. To help simplify this essential step in the homebuying procedure, right here's a breakdown of the 3 most common loan choices readily available from banks and credit unions. Department of Veterans Matters to aid solution participants, experts as well as qualified surviving spouses. A good home loan broker or home loan banker should be able to help guide you with all the different programs and options, yet nothing will certainly offer you far better than recognizing your top priorities for a mortgage loan.

What Do You Intend to Make With Your Cash?

Suitable for debtors with previous credit concerns and also those looking for down payment and closing expense assistance programs. A house equity line of credit, or HELOC, acts somewhat like a bank card, utilizing your home as collateral.

When you're starting out, traditional residence finances are possibly not an alternative for purchasing financial investment buildings-- at least. However, if you're going to inhabit the house as your primary residence as well as you can adjust to the troubles listed below, mortgage loans might work.